As 2014 approaches, major changes are coming with the Affordable Care Act (ACA) also knows as Obamacare. There are many more options for startups – both in terms of plans, payments, and public exchanges. Here’s what you really need to know in the coming months:

What happens when the Exchanges open on October 1?

State exchanges are online marketplaces where you can purchase health insurance for yourself or your business. New plan options will be available in each state. SimplyInsured has created a handy guide – explaining the plans of pricing of the new options:

Plans will be available in four flavors – Bronze, Silver, Gold and Platinum – with increasing levels of cost and coverage. Unfortunately, not all insurance companies will be offering individual or small business plans through the exchange.

| Insurance Companies participating in CA Exchange | |||

|---|---|---|---|

| Participating | Not Participating | ||

The individual exchanges will open on October 1, 2013 so you can start looking at plans. Small businesses should be able to see plans on the exchanges, though those exchanges are facing potential delays in some states.

OUR ADVICE:

- First – get a sample quote from the new exchange here: http://www.simplyinsured.com/covered-california-standard-plans

- Next – compare these options to other available options that are NOT on the exchange: http://www.simplyinsured.com/small-group/first-quote

- Lastly – make sure your employees know of their options, and they can make the best decisions for their individual coverage.

Do I still need a broker even though there’s an exchange?

Yes! Having a broker will make healthcare easier for you, and it’s free! State exchanges only meet a subset of your company’s needs. Using SimplyInsured as your broker gives you substantial benefits at no additional cost.

| State Exchanges | Traditional Broker | SimplyInsured | |

|---|---|---|---|

| Purchase of health insurance plans | |||

| Purchase of dental and vision plans | |||

| Online application process | |||

| Access to all available plans | |||

| Online Employer Dashboard | |||

| Online Employee Tools | |||

| Payroll Integration and Automation | |||

| Insurance Dispute Resolution and Advocacy |

So, what’s changing on January 1, 2014?

The main change is the “Individual Mandate”. The Individual Mandate states – that all individuals will need to have a minimum level of health insurance coverage or face fines. These fines can be thousands of dollars and will increase through 2016. Details on fines can be found here:

https://www.healthcare.gov/what-if-someone-doesnt-have-health-coverage-in-2014/

Groups insured through SimplyInsured will not face these fines. We ensure your plan is compliant with your state’s minimum coverage requirement and other regulation.

Will my rates go up?

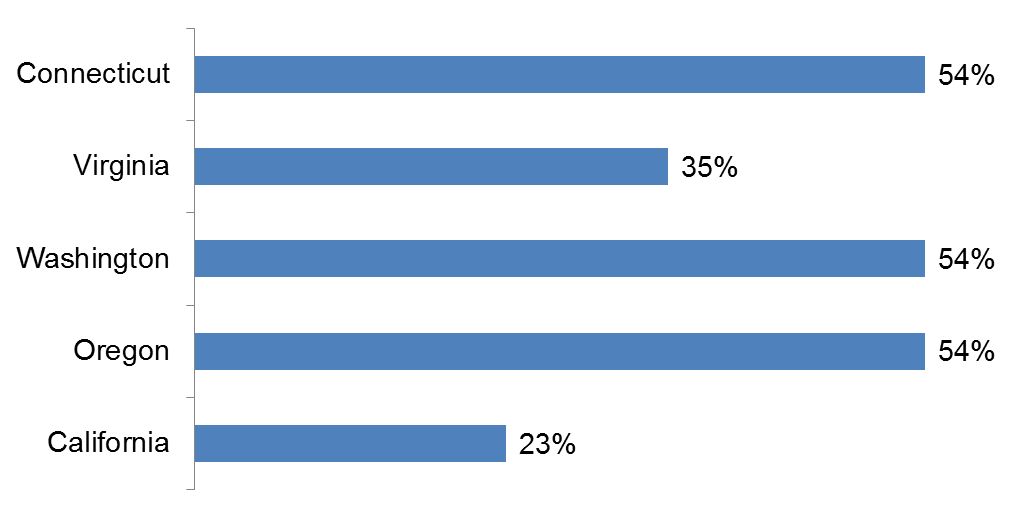

Yes, especially if you are under 30 years old and healthy. With insurance companies unable to deny coverage to people with pre-existing conditions, they need to increase rates across the board to cover their increased costs. In many states, premiums are expected to increase by 15-50% for people under 40 years of age.

AVERAGE 2014 PREMIUM INCREASE:

| Age 27 | Age 40 |

|

|

Your can find information for other states using this interactive map tool.

OUR ADVICE:

Lock in your rates before January 1. Insurance companies are offering renewal specials, allowing lock-in at lower rates through January 1st. Your broker should help you take advantage of these offers. To find the lowest renewal rates for your small business, get a free quote here: www.simplyinsured.com.

Will I face additional regulation?

Most regulations on small businesses have been delayed to 2015. The most significant change coming in 2014 is a change to the small business tax credit. To be able to claim the credit, you must:

- Have less than 25 FTEs

- Pay your employees an average wage of $50K or less

- Pay 50% or more of your employees’ premiums

- Secure a plan offered through the exchange

CALCULATE YOUR POTENTIAL TAX SAVINGS:

| Health Insurance Tax Credit Calculator (2013) | |

|---|---|

| Monthly Premium per Employee ($) | |

| Number of Employees (#) | |

| Avg. Employee Wages per Year ($) | |

| Tax Credit (calculate) | – |

What if I can’t afford insurance for myself or my employees?

The exchanges will offer premium subsidies for lower-income individuals. For individuals making less than $28,725 per year – subsidies range from 5% to 95% of medical premiums for “Silver” rated exchange plans. The Kaiser Foundation has created a calculator to estimate if you qualify:

Am I required to offer health insurance to my employees?

No, if you have less than 50 employees. However, your employees may face fines if they do not have health insurance.. Many employees will look to their employers for health insurance.

What should I do to prepare for the coming of the ACA?

Individuals:

- Check with your provider to ensure your insurance will be offered in 2014 and get your renewal price

- Compare prices with your state’s individual exchange on October 1

- Ask your employer if they plan to offer coverage starting next year

Businesses:

- Check SimplyInsured to find the best value health insurance plan.

- Ask your broker about early renewal specials to lock in lower rates.

- Check SimplyInsured in October to see if there’s a better plan option through the exchanges.